Three weeks into restricted global trade through the Strait of Hormuz, the corn industry has a clearer picture of how fertilizer markets are reacting, not just in futures contract prices but also at the retail level. This provides a basis for understanding how farmers and the new corn crop will be impacted by this shock on the brink of planting season.

Immediate Price Reactions: Fertilizer Futures Spike

Several fertilizer products trade as Chicago Board of Trade (CBOT) commodities, which means prices can react in real time, indicating how markets are responding to global geopolitical developments. Urea showed an immediate move following the start of the war: the nearby Gulf Free-On-Board (FOB) March 2026 contract jumped $128 per ton between February 27 and March 3.

The May 2026 urea contract rose more slowly at first, but the rally then continued ahead. The contract’s March 19 close of $681 per ton is an increase of $276 per ton (68%) from the end of February. At $681 per ton, urea is elevated but not at a record high. In April 2022, prices surpassed $1,000 per ton.

Since the end of February, the Gulf FOB April 2026 contract for diammonium phosphate (DAP) has increased $40 per ton (6%). The move is smaller than the price response seen in urea contracts, but is still concerning given DAP’s sustained high price level in recent years. DAP prices were already relatively high prior to the Strait of Hormuz constraints, reflecting existing market supply restrictions. Like urea, DAP reached highs of $1,000 per ton in 2022, and prices have been slow to decline from their peak. Before the hikes seen in March 2026, DAP was persistently pricing at $600 per ton, while urea had fallen over time to below $500 per ton.

Retail Fertilizer Prices Catch-Up

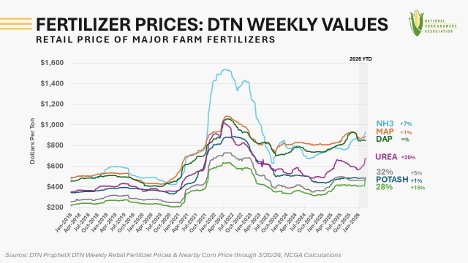

Movement in contract prices is a useful indicator of wholesale market pricing, or what global buyers and sellers agree upon for a stated period, that can be tracked in real time. The prices farmers actually pay to purchase fertilizers is more difficult to track as it varies widely by location and is backward looking. For example, the USDA Illinois Production Cost Report, a bi-weekly publication reporting retail prices for fuel and fertilizer over the previous period, showed a much weaker response in the first week of the conflict compared to what was being traded on barges in New Orleans but showed a significant jump in prices (especially urea) in the week ending 3/20/26. Another resource, the DTN Retail Fertilizer Index, a weekly average of retail fertilizer prices from across the nation, similarly lagged the dramatic support seen in the futures markets immediately following the market shock, but also reflected moderated price impacts at the national level compared to the regional focus of the Illinois report.

Illinois Cost Production Report (Bi-Weekly)

| Week Ending2/20 | Week Ending3/6 | Week Ending3/20 | Change Sinceend of Feb | |

| DAP | $828 | $833 | $841 | $13/ton (2%) |

| Urea | $581 | $591 | $823 | $242/ton (42%) |

| Anhydrous Ammonia | $843 | $903 | $998 | $155/ton (18%) |

| No. 2 Diesel | $3.14 | $3.90 | $4.23 | $1.09/gal (35%) |

DTN Retail Fertilizer Index

| Week Ending 2/20 | Week Ending3/6 | Week Ending 3/20 | Change Sinceend of Feb | |

| DAP | $852 | $850 | $851 | $-1/ton (0%) |

| Urea | $608 | $625 | $677 | $69/ton (11%) |

| Anhydrous Ammonia | $862 | $895 | $931 | $69/ton (8%) |

Big Picture Perspective of a Dynamic Situation

As numbers trickle in to shape our understanding of both global fertilizer markets and how this event will shape farmer decision-making at a critical point, under already-tough conditions, taking a step back to look at trends helps characterize how this situation will be felt in the farm economy.

In what seems to be a trend for recent years, there is much chatter about this being an ‘unprecedented’ event, with the closest parallel on a fertilizer price chart being the spikes following the 2022 Russian invasion of Ukraine. However, while the impacts of that event are certainly still reverberating through fertilizer markets today, there are a few key contrasts that make the current situation different and difficult to draw an analog year. Retail prices for ammonia at the height of that global event peaked at about $1,300/ton in 2022, and in March 2026, though prices are relatively high, a ton costs about $900. Other fertilizer products reached higher absolute values as well.

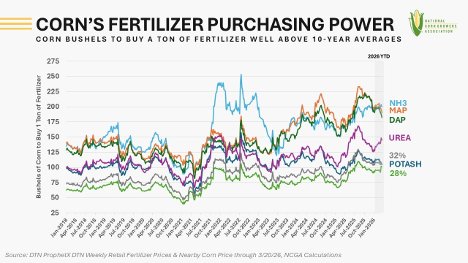

However, a fundamental difference between that situation and current situation unfolding on the farm was the commensurate price of agricultural commodities. As Russia and Ukraine are both major exporters of grain, corn prices spiked to near-records in the U.S. as a result of the geopolitical turmoil. Today, as the Middle East is a net-importer of grains, we have not seen a commensurate increase in the price of corn, as most upward support has been provided by energy moves or new crop speculation. In 2022, corn reached $8 per bushel. Today, the nearby (May 2026) corn contract is about $4.70 per bushel. The relationship between these two commodities is an important indicator of how market conditions will be felt in the farm economy. Looking at the decisions farmers are facing right now, current May contract prices it takes roughly 145 bushels of corn to buy one ton of urea versus about 125 bushels in April 2022—even though the urea Gulf FOB price was nearly 50% higher at the time.

Bringing it Back to the Farm Gate: Middle East Spike Latest in Trend of Declining Fertilizer Affordability

To put the relationship between corn and fertilizer prices into the context of the farm level and the conditions of the agricultural economy to weather this latest event, the graph above shows corn bushels needed to buy a ton of fertilizer at the retail price over time. As can be seen, fertilizer has been high in the price of corn for an extended period before the further dramatic spikes of the beginning of March, particularly for anhydrous ammonia and phosphate products.

This trend unsurprisingly coincides with the fourth straight year of projected negative returns, challenging the liquidity and cash flow needed to purchase inputs that are not only more expensive in absolute terms, but also in the “price” of corn- putting the average grower in a tight financial situation on the farm even before March 2026 and Intensifying the impact of the Strait of Hormuz closure.

Farmer Fallout: Concerns Carry to 2027

Rounding out the third week of the Strait of Hormuz disruption, fertilizer price risk is becoming clearer. Futures markets have moved quickly, with nitrogen posting an immediate jump and continuing higher, while phosphate prices remain concerning given existing high prices. Retail prices are still catching up because current sales reflect inventory bought before March, but that buffer is temporary; as retailers restock at higher replacement values, farm-gate fertilizer prices are likely to rise further. Unlike the 2022 fertilizer price spike, corn price is not providing the same revenue offset, increasing the odds that producers who still need to acquire fertilizer supplies adjust application rates or adapt planting plans to protect cash flow.

Looking ahead, NCGA continues to warn that phosphate countervailing duty measures effectively tighten the U.S. supply picture and contribute to higher phosphate prices at the farm gate. That matters now—but it matters even more for 2027. If policy decisions keep import volumes constrained while global risks remain elevated, corn growers could enter the 2027 season facing even higher costs. With many growers already facing tight margins, the bigger risk is that today’s policy-driven constraints become tomorrow’s availability problem, particularly as the global market is operating under very tight supply conditions. Corn producers will need reliable, competitively priced fertilizer for 2027 crop plans, and NCGA’s position reflects a straightforward concern: without a more open and resilient supply channel, elevated prices—and potential shortages—could carry forward into the next buying cycle.

Story originally published by the National Corn Growers Association.